⚖️ For Fairness Sake ⚖️ QAD acquired by Thoma Bravo for ~$1.8bn

A quick look at QAD's fairness opinion

QAD acquired by Thoma Bravo for ~$1.8 billion.

This is a little more preliminary look since the PREM14A with the fairness was just filed and we are missing a lot of data that may get filled in. I will likely update this post as we get more data.

QAD / Thoma Bravo deal overview

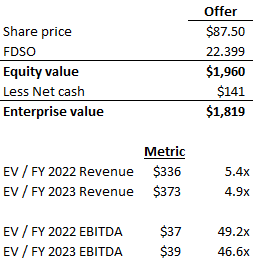

June 28, 2021 – QAD (Nasdaq: QADA and QADB), a leading provider of next-generation manufacturing and supply chain solutions in the cloud, announced that it has entered into a definitive agreement to be acquired by Thoma Bravo, Fund XIV, in an all-cash transaction with an equity value of approximately $2 billion. Under the terms of the agreement, QAD shareholders will receive $87.50 per share of Class A Common Stock or Class B Common Stock in cash.

Following the completion of the deal, expected in the fourth quarter of 2021, QAD founder and President Pamela Lopker will retain a significant ownership interest in the company and continue to serve on the board.

QAD Class B common stock has one vote per share and Class A common stock has 1/20th vote per share. Stockholders who hold shares of our Class B common stock collectively have approximately 79% of the voting power of our outstanding capital stock as of January 31, 2021. As of January 31, 2021, Pamela Lopker beneficially owned approximately 31% of the outstanding shares of our Class A common stock and approximately 77% of the outstanding shares of our Class B common stock, representing approximately 67% of the voting power of our outstanding capital stock.

Termination Fee equal to $59,000,000 (3.0% of equity value)

Reverse Termination Fee equal to $127,000,000 (6.5% of equity value)

Background of the merger

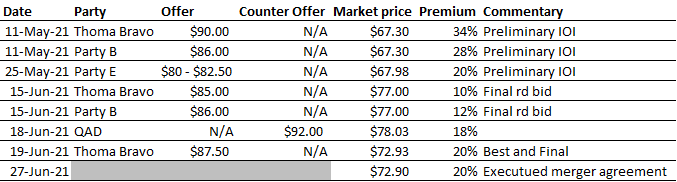

TL;DR: During 2019 and 2020, the QAD discussed a potential review of strategic alternatives for QAD. In February 2021, QAD decided to run a formal sale process. Ms. Lopker, the President and founder of QAD, also expressed her willingness to pursue a process, her openness to consider any type of transaction, and her preference for retaining an ongoing stake in the Company. From mid-March 2021 to early May 2021, Morgan Stanley contacted over 25 potential counterparties, including both potential strategic counterparties and financial sponsors, to gauge their interest in potential transactions with QAD. During this period, QAD entered into 18 confidentiality agreements with interested parties. QAD requested preliminary indications of interest by May 11, 2021 and only Thoma Bravo and Party B submitted IOIs. Party E ended up submitting at IOI of $80 to $82.50 per share, but would not go any higher. QAD requested final bids by June 15, 2021, TB came in with a lower offer of $85, than its first IoI after diligence, but was convinced to increase its offer to $87.50 with no debt financing. Party B offered $86, but was ultimately unwilling to raise its offer.

Offer timeline

The wringer

QAD filed a PREM14A on August 2, 2021 that contained Morgan Stanley’s fairness opinion. MS delivered an oral and written opinion to the BoD on June 27, 2021. The initial submission is missing a lot of key financial data need to recreate the analysis, we will see if Investors sue to get more disclosure.

QAD has agreed to pay Morgan Stanley a fee of approximately $27 million for its services, $3 million of which has been paid following delivery of the opinion described in this section and attached to this proxy statement as Annex D and the remainder of which is contingent upon the consummation of the Merger

It is fair to MS. This works out to ~1.5% of the $1.8 billion enterprise value, which would probably be at the high end of M&A sell-side fee tables.

For its fee, MS goes with the standard valuation methods and some for observation only.

Trading comparables

Transaction comparables

DCF

Discounted Equity

Illustrative Precedent Premiums

Historical Trading Ranges

Equity Research Analysts’ Future Price Targets

A few caveats before we begin diving into the numbers. I am not going to be able tie out all the share price ranges due to several factors:

Financials projections are rounded to the ones

Quarterly projections not provided

A full option schedule was not provided in any filings

No FCF or line items to calculate FCF provided

Projected share count and net debt for discounted equity analysis not provided

Again, the old saying still applies, “you get what you pay for” and this is free. That said, we are in the ballpark for all analysis, so let’s dive in.

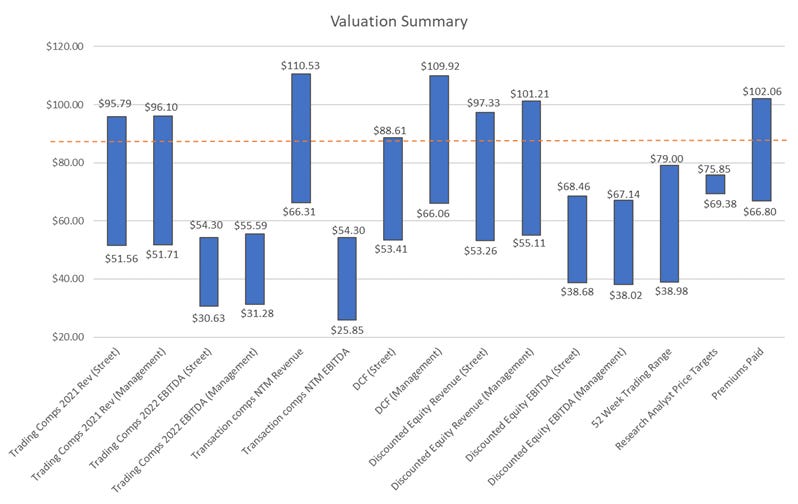

Valuation Summary

Is it Fair?

As my Beekeeper used to say, only God and the Delaware Courts can decide that.

Pamela Lopker beneficially owned ~31% of the Class A and ~77% of the Class B stock, representing ~67% of the voting power

QAD ran a full formal sale process

20% premium is probably just high enough to make the offer compelling

Offer is above the 52 week high and stock had been performing relatively well

Offer is above EBITDA based valuation metrics but below Revenue based valuation metrics

Management projected financials

(1) For the purposes of the financial analyses as described above under the heading “— Opinion of Morgan Stanley & Co. LLC,” fiscal year projections are treated as the prior calendar year projections (e.g., FY2022E (ended January) is equivalent to CY2021E (ended December)).

(2) Adjusted EBITDA is a non-GAAP measure. Our calculation of Adjusted EBITDA may differ from other companies and excludes the following items: interest, income taxes, depreciation and amortization, restructuring, separation, transaction and integration-related cost and other non-recurring items. Adjusted EBITDA differs from Reported Adjusted EBITDA because Reported Adjusted EBITDA does not include expenses associated with stock-based compensation.

Summary valuation

Discounted Cash Flow Analysis

Morgan Stanley utilized estimates from the Street Case and Management Case for purposes of its discounted cash flow analysis, as more fully described below.

Morgan Stanley first calculated the estimated unlevered free cash flow, which is defined as EBITDA less (1) stock-based compensation expense, (2) cash taxes, (3) capital expenditures, and plus or minus changes in net working capital. Each of the Street Case and Management Case included extrapolations through calendar year 2030 prepared by Morgan Stanley and approved for Morgan Stanley’s use by QAD’s management. The free cash flows and terminal values were discounted, using a mid-year convention, to present values as of June 30, 2021, at a discount rate ranging from 7.1% to 9.1%, which discount rates were selected, upon the application of Morgan Stanley’s professional judgment and experience, to reflect an estimate of QAD’s weighted average cost of capital determined by the application of the capital asset pricing model. Morgan Stanley utilized perpetual growth rates of 2.0% to 3.0% as part of its analyses, with such rates selected upon the application of Morgan Stanley’s professional judgment and experience. The resulting aggregate value was then adjusted for net cash and further adjusted for the net present value of net operating losses.

Based on the outstanding Share on a fully diluted basis as provided by QAD’s management, Morgan Stanley calculated the estimated implied value per Share as follows:

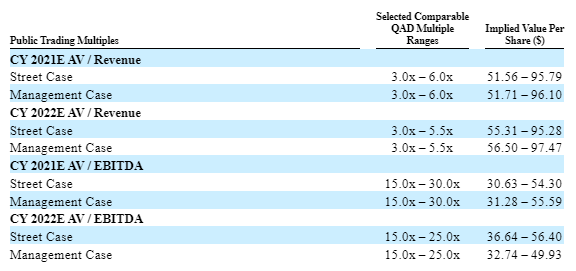

Selected Companies Analysis

Morgan Stanley performed a public trading comparables analysis, which attempts to provide an implied value of a company by comparing it to similar companies that are publicly traded. Morgan Stanley reviewed and compared certain financial estimates for QAD with comparable publicly available consensus equity analyst research estimates for companies, selected based on Morgan Stanley’s professional judgment and experience, that share similar business characteristics and have certain comparable operating characteristics, including, among other things, similarly sized revenue and/or revenue growth rates, market capitalizations, profitability, scale and/or other similar operating characteristics (these companies are referred to as the “comparable companies”). These companies were the following:

ERP Business Model Peer Companies

Oracle Corporation

SAP SE

Sage Group plc

Financial Profile Peer Companies

Vertex Software, LLC

Zuora Inc.

Alarm.com

New Relic, Inc.

8x8, Inc.

Box, Inc.

GoDaddy Inc. Yext Inc.

Vonage Holdings Corp.

Teradata Corporation

Global Supply Chain Peer Companies

Manhattan Associates, Inc.

Descartes Systems Group Inc.

Kinaxis Inc.

SPS Commerce, Inc.

E2open, LLC

For purposes of this analysis, Morgan Stanley analyzed the ratio of aggregate value to (i) estimated revenue and (ii) EBITDA, both of which, for purposes of this analysis, (a) for QAD, (x) were provided to Morgan Stanley, and approved for Morgan Stanley’s use, by QAD’s management for calendar years 2021 and 2022 for the Management Case, and (y) were based on the median of publicly available equity analyst research estimates for calendar years 2021 and 2022 for the Street Case; and (b) for each of the comparable companies, were based on publicly available consensus equity analyst research estimates for comparison purposes. For purposes of its analyses, Morgan Stanley defined “aggregate value” as a company’s fully diluted equity value plus total debt, plus non-controlling interest, less cash and cash equivalents, and “EBITDA” as earnings before interest, taxes, depreciation and amortization of intangible assets.

Based on its analysis of the relevant metrics for each of the comparable companies and upon the application of its professional judgment and experience, Morgan Stanley selected representative ranges of (i) aggregate value to estimated revenue multiples and (ii) aggregate value to estimated EBITDA multiples, and applied these ranges of multiples to the estimated relevant metric for QAD. For purposes of this analysis, Morgan Stanley utilized publicly available financial information, available as of June 25, 2021 (the last full trading day prior to the meeting of the QAD Board (other than Ms. Lopker, who recused herself) to approve and adopt the Merger Agreement, declare the advisability of the Merger Agreement and approve the transactions contemplated thereby, including the Merger).

Based on the outstanding Shares on a fully diluted basis as provided by QAD’s management, Morgan Stanley calculated the estimated implied value per Share as follows:

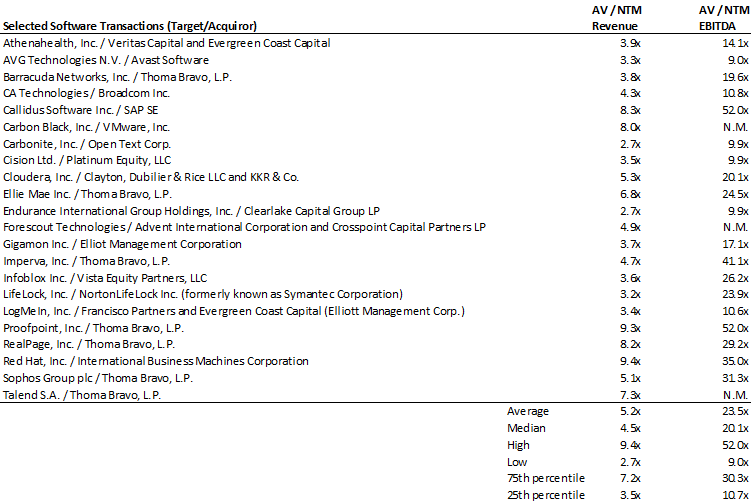

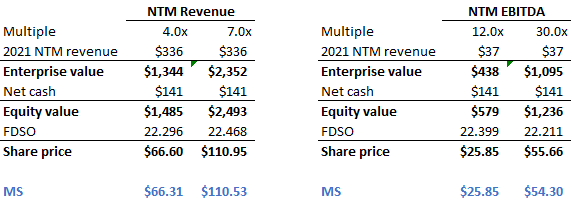

Selected Transactions Analysis

Morgan Stanley performed a precedent transactions multiples analysis, which is designed to imply a value of a company based on publicly available financial terms. Morgan Stanley selected such comparable transactions because they shared certain characteristics with the Merger, most notably because they were similar software transactions. For such transactions, Morgan Stanley noted the multiple of aggregate value of the transaction to (i) the estimated next twelve (12) months’ (which we refer to as “NTM”) revenue, and (ii) the NTM EBITDA, each based on publicly available information at the time of announcement of each such transaction.

The following is a list of the selected software transactions reviewed, together with the applicable multiples:

Based on its analysis of the relevant metrics and time frame for each of the transactions listed above and upon the application of its professional judgment and experience, Morgan Stanley selected representative ranges of the aggregate value to the (i) estimated NTM revenue multiples of the transactions and (ii) estimated NTM EBITDA multiples of the transactions, and applied these ranges of multiples to the estimated calendar year 2021 NTM revenue and NTM EBITDA, respectively, based on the Street Case. The following table summarizes Morgan Stanley’s analysis:

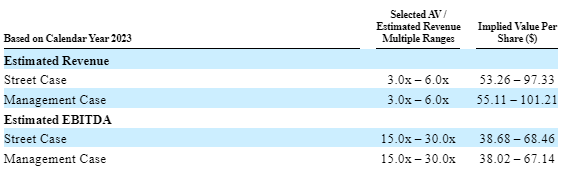

Discounted Equity Value Analysis

Morgan Stanley performed a discounted equity value analysis, which is designed to provide insight into the potential future equity value of a company as a function of such company’s estimated future revenue and EBITDA. The resulting equity value is subsequently discounted to arrive at an estimate of the implied present value. In connection with this analysis, Morgan Stanley calculated a range of implied present equity values per Share on a standalone basis for each of the Street Case and Management Case.

To calculate these discounted fully diluted equity values, Morgan Stanley utilized (i) calendar year 2023 revenue estimates and (ii) calendar year 2023 EBITDA estimates under each of the Street Case and Management Case, respectively. Based upon the application of its professional judgment and experience, Morgan Stanley applied a forward range of aggregate value to (i) estimated revenue multiples, and (ii) EBITDA multiples (based on the range of aggregate value to revenue and EBITDA multiples for the comparable companies) to these revenue and EBITDA estimates, respectively, in order to reach a future implied fully diluted equity value.

In each case, Morgan Stanley then added net cash to QAD’s future implied aggregate value to reach a future implied fully diluted equity value. In each case, Morgan Stanley then divided the future implied fully diluted equity value by estimated fully diluted shares outstanding (with such estimates provided by QAD management) to calculate a per share price. Morgan Stanley then discounted the resulting implied future share price to June 30, 2021, at a discount rate of 8.1%, which rate was selected based on QAD’s estimated cost of equity, which was arrived at by applying the capital asset pricing model, to calculate the discounted fully diluted equity value.

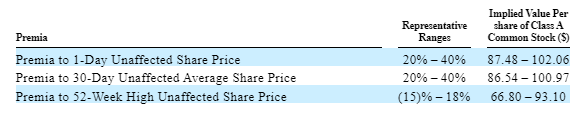

llustrative Precedent Premiums

Morgan Stanley performed an illustrative precedent premiums analysis by reviewing the same sets of comparable transactions as under the Precedent Transactions Multiples Analysis. For these transactions, Morgan Stanley noted the distributions of the following financial statistics, where available: (1) the implied premium to the acquired company’s closing share price on the last trading day prior to announcement (or the last trading day prior to the share price being affected by acquisition rumors or similar merger-related news); (2) the implied premium to the acquired company’s thirty (30)-trading-day average closing share price prior to announcement (or the last thirty (30)-trading-day average closing share price prior to the share price being affected by acquisition rumors or similar Merger-related news); and (3) the implied premium to the acquired company’s fifty two (52)-week high closing share price prior to announcement.

Based on its analysis of the premia for such transactions and based upon the application of its professional judgment and experience, Morgan Stanley selected a representative range of premia and applied such range to QAD’s closing share price of Class A Common Stock on June 25, 2021 (the last full trading day prior to the meeting of the QAD Board (other than Ms. Lopker, who recused herself) to approve and adopt the Merger Agreement, declare the advisability of the Merger Agreement and approve the transactions contemplated thereby, including the Merger).

The following table summarizes such calculation:

Historical Trading Ranges

Morgan Stanley noted certain trading ranges with respect to the historical share prices of Class A Common Stock. Morgan Stanley reviewed a range of closing prices of the Class A Common Stock for various periods ending on June 25, 2021 (the last full trading day prior to the meeting of the QAD Board (other than Ms. Lopker, who recused herself) to approve and adopt the Merger Agreement, declare the advisability of the Merger Agreement and approve the transactions contemplated thereby, including the Merger). Morgan Stanley observed the following:

Equity Research Analysts’ Future Price Targets

Morgan Stanley noted certain future public market trading price targets for Class A Common Stock prepared and published by equity research analysts prior to June 25, 2021 (the last full trading day prior to the meeting of the QAD Board (other than Ms. Lopker, who recused herself) to approve and adopt the Merger Agreement, declare the advisability of the Merger Agreement and approve the transactions contemplated thereby, including the Merger). These targets reflected each analyst’s estimate of the future public market trading price of Class A Common Stock. The range of undiscounted analyst price targets for the Class A Common Stock was $75.00 to $82.00 per share as of May 26, 2021 to May 27, 2021. Morgan Stanley discounted the range of analyst price targets per share of Class A Common Stock by one (1) year at a rate of 8.1%, which discount rate was selected by Morgan Stanley, upon the application of its professional judgment and experience, to reflect QAD’s cost of equity. This analysis indicated an implied range of fully diluted equity values for shares of Class A Common Stock of $69.38 to $75.85 per share, as discounted by one (1) year based on undiscounted analyst price targets, as of June 25, 2021 (the last full trading day prior to the meeting of the QAD Board (other than Ms. Lopker, who recused herself) to approve and adopt the Merger Agreement, declare the advisability of the Merger Agreement and approve the transactions contemplated thereby, including the Merger).

Background of the Mergers

On February 9, 2021, the QAD Board and its legal counsel, Manatt, Phelps & Phillips, LLP, which we refer to as Manatt, met to discuss, among other things, a potential review of strategic alternatives for QAD. After discussion and deliberation, the independent members of the QAD Board determined to request that senior management of QAD meet with representatives of Morgan Stanley in to provide their views regarding recent developments in the software industry and potential strategic options for the Company.

On February 18, 2021, Ms. Lopker, the President and founder of QAD, Mr. Anton Chilton, the Chief Executive Officer of QAD, and Mr. Daniel Lender, the Chief Financial Officer of QAD, met with representatives of Morgan Stanley to review potential strategic alternatives for QAD.

Over the following days, after discussion and deliberation, the members of the QAD Board executed a unanimous written consent, effective as of February 21, 2021, to form the Special Committee, with Mr. van Cuylenburg, Mr. Scott Adelson, Ms. Kathy Crusco and Mr. Lee Roberts as its members. The QAD Board determined each member of the Special Committee to be unaffiliated with, and otherwise independent from, Ms. Lopker and to be otherwise independent and disinterested with respect to the Special Committee’s mandate.

During this same period, members of the Special Committee recommended to Ms. Lopker that she retain independent financial and legal advisors. Ms. Lopker also expressed to such members her willingness to pursue a process, her openness to consider any type of transaction, and her preference for retaining an ongoing stake in the Company.

On March 8, 2021, the Special Committee met and, after discussion and deliberation, approved the selection of Paul, Weiss, Rifkind, Wharton & Garrison LLP, which we refer to as Paul, Weiss, as legal counsel to the Special Committee. The Special Committee selected Paul, Weiss based, in part, on its experience representing special committees in circumstances similar to that of the Special Committee. At this meeting, the Special Committee also appointed Messrs. van Cuylenburg and Adelson as co-chairs of the Special Committee.

On March 15, 2021, representatives of Morgan Stanley provided the Special Committee a preliminary overview of potential strategic alternatives for QAD. Morgan Stanley also disclosed its relationships with respect to several potential counterparties. Also during such meeting, representatives of Morgan Stanley confirmed that it had not performed any work or services for Ms. Lopker, nor had it provided any financial analysis regarding QAD to any third party. The members of the Special Committee and representatives of Paul, Weiss had further discussions in an executive session.

Thereafter, and after further discussion and deliberation, the Special Committee determined to engage Morgan Stanley as its financial advisor, based in part, on Morgan Stanley’s qualifications, expertise and reputation, its knowledge of and involvement in recent transactions in QAD’s industry, and its knowledge of QAD’s business and affairs, with such engagement being formalized in a written engagement letter dated March 30, 2021.

During the period from mid-March 2021 to early May 2021, at the direction of the Special Committee, representatives of Morgan Stanley contacted over 25 potential counterparties, including both potential strategic counterparties and financial sponsors, to gauge their interest in potential transactions with QAD. During this period, QAD entered into 18 confidentiality agreements with interested parties. None of these confidentiality agreements included any standstill provisions.

Representatives of Morgan Stanley, along with Messrs. Chilton and Lender, met with representatives of all 18 parties that signed confidentiality agreements to provide background regarding QAD and its financial performance.

On May 3, 2021, After review and deliberation, the Special Committee directed representatives of Morgan Stanley to send a process letter to such parties containing bid instructions and procedures (the form of which was approved by the Special Committee) and to request preliminary indications of interest by May 11, 2021. Over the course of the following weeks, representatives of Morgan Stanley, together with Messrs. Chilton and Lender, continued to participate in due diligence discussions upon the request of the potential counterparties involved in the process.

Also on May 3, 2021, the Special Committee discussed with its advisors outreach to additional potential counterparties. At the direction of the Special Committee, representatives of Morgan Stanley then proceeded to contact two additional potential counterparties, which we refer to as Party C and Party D, to gauge their interest in participating in the process.

On May 11, 2021, on behalf of the Special Committee, representatives of Morgan Stanley received written preliminary, non-binding indications of interest from two of the eight parties who had been sent a process letter, which indications were promptly provided to the Special Committee and its advisors. The two parties who submitted preliminary indications of interest were Thoma Bravo and a party we refer to as Party B. Thoma Bravo’s indication of interest outlined a potential transaction in which QAD stockholders would receive up to $90 per share in cash, subject to further due diligence and negotiations, which cash consideration would be financed with a mixture of debt and equity. Thoma Bravo’s indication of interest independently raised the possibility of Ms. Lopker continuing to hold a portion of her interests in QAD by rolling over a percentage of her holdings and also expressly stated that, in connection with its diligence, Thoma Bravo representatives would require discussions with Ms. Lopker regarding her involvement in the Company following the closing of the proposed transaction. Party B’s indication of interest outlined a potential transaction in which QAD stockholders would receive approximately $86 per share in cash, subject to further due diligence and negotiations, which cash consideration would be financed with a mixture of debt and equity. Party B also verbally indicated to representatives of Morgan Stanley its request to meet with Ms. Lopker to discuss her involvement in the Company following the closing of the proposed transaction. Both Thoma Bravo and Party B indicated to representatives of Morgan Stanley that they would each require a support agreement in connection with any transaction, which would require, among other things, that the Lopker Entities vote in favor of the contemplated transaction (subject to certain exceptions) with the relevant counterparty.

Four of the eight parties that received the process letter expressed to representatives of Morgan Stanley potential interest in a transaction with QAD at a “low-to-no premium” value over the then-current publicly traded price per share, but did not submit any indications of interest. The remaining two parties who had received a process letter expressed to representatives of Morgan Stanley potential interest in a private investment in public equity transaction with QAD, but did not submit indications of interest. On May 11, 2021, QAD’s closing share price of Class A Common Stock was $67.30.

The Special Committee reiterated that Messrs. Chilton and Lender were not to have any discussions relating to information learned in a Special Committee meeting with anyone, including Ms. Lopker, without the permission of the Special Committee, and added that no one other than members of the Special Committee were to discuss the process or preliminary indications of interest with Ms. Lopker at that stage. The members of the Special Committee and representatives of Paul, Weiss had further discussion during an executive session of the meeting. After review and deliberation, the Special Committee determined to seek additional details from each of Thoma Bravo and Party B regarding their respective preliminary indications of interest.

Also on May 14, 2021, Messrs. van Cuylenburg and Adelson met with Ms. Lopker to provide her with the high-level terms of the preliminary indications of interest received from each of Thoma Bravo and Party B. Ms. Lopker indicated that she was interested in continuing to have a role in QAD following the closing of a potential transaction if one were to occur, and that she was open to discussions with each of Thoma Bravo and Party B about such role. Ms. Lopker indicated that she had not yet decided whether she would seek a rollover of a portion of her shares in QAD.

On May 17, 2021, After discussion and deliberation, representatives of Morgan Stanley confirmed that, at the direction of the Special Committee, they would request that any remaining parties in the process submit indications of interest by May 25, 2021.

On May 19, 2021, and on May 21, 2021, Ms. Lopker had initial discussions with each of Party B and Thoma Bravo, respectively, with representatives of Morgan Stanley present, to discuss Ms. Lopker’s potential involvement in QAD following the closing of a potential transaction with each such counterparty. No discussion of any specific terms of such an arrangement, or a potential rollover of a portion of Ms. Lopker’s shares in QAD, took place. Following these meetings, Ms. Lopker indicated to Messrs. Adelson and van Cuylenburg that she was open to further discussion with both of Thoma Bravo and Party B.

On May 25, 2021, of the seven potential counterparties who had been sent a process letter, Morgan Stanley received one additional written non-binding preliminary indication of interest, from two parties who partnered together, which we refer to collectively as Party E. Such indication of interest included a range of $80 to $82.50 per share, as well as a list of outstanding diligence items, and stated that any transaction would be financed with a mix of debt and equity. Such indication of interest was promptly provided to the Special Committee and its advisors. On May 25, 2021, QAD’s closing share price of Class A Common Stock was $67.98.

On May 26, 2021, the Special Committee directed representatives of Morgan Stanley to inform Party E that the price included in its indication of interest was too low and it would need to increase its offer price per share in order to proceed in the process.

At that same meeting, Representatives of Morgan Stanley advised that certain of such parties indicated that they may be interested in an at-market transaction with QAD, and were not willing to offer any premium to the then-current publicly-traded market price. On May 26, 2021, QAD’s closing share price of Class A Common Stock was $67.64.

Also at that meeting, the Special Committee discussed with its advisors outreach to additional potential counterparties. At the direction of the Special Committee, representatives of Morgan Stanley then proceeded to contact two additional potential counterparties, which we refer to as Party F and Party G, to gauge their interest in participating in the process.

On May 28, 2021, Morgan Stanley followed-up with Party D, which had not submitted any indication of interest, and encouraged Party D to continue considering a potential transaction with QAD. Party D indicated that it would no longer be participating in the process.

On June 1, 2021, QAD entered into a confidentiality agreement with Party F. Such confidentiality agreement did not include any standstill provisions.

On June 2, 2021, Party C notified representatives of Morgan Stanley that it would no longer be participating in the process.

On June 7, 2021, Representatives of Morgan Stanley stated that, after they had contacted Party E to relay the Special Committee’s message that Party E would need to increase its price in order to proceed in the process, Party E had responded that it would not increase its price, and that Morgan Stanley should notify it if circumstances change and there would be an opportunity to move forward in Party E’s proposed price range of $80 to $82.50 per share.

At that same meeting, the Special Committee and its advisors further discussed the status of Thoma Bravo, Party B and the other two remaining parties in the process. After discussion and deliberation, the Special Committee directed Morgan Stanley to communicate to all parties remaining in the process to submit final proposals with respect to a potential transaction with QAD by June 15, 2021.

Also during that same meeting, the Special Committee and its advisors discussed the potential terms of a draft merger agreement that was to be provided to bidders in connection with soliciting bids. The draft expressly stated that if Ms. Lopker seeks to participate in a rollover of any of her shares, then, in addition to the stockholder vote required by Delaware law, the Special Committee would further require that the majority of QAD’s disinterested stockholders also approve the transaction. The Special Committee and its advisors discussed that this “majority of the minority” vote would be a non-waivable condition for the transaction, and that such vote requirement would also be communicated to Ms. Lopker in the event she sought to roll over any of her shares of QAD. The Special Committee and its advisors also discussed the terms of a support agreement, which would require, among other things, that the Lopker Entities vote in favor of the contemplated transaction with the relevant counterparty (subject to certain exceptions), which the parties participating in the process had continued to indicate they would require in connection with a potential transaction. The members of the Special Committee and representatives of Paul, Weiss had further discussion during an executive session of the meeting.

On June 7, 2021, Party F notified representatives of Morgan Stanley that it would no longer be participating in the process.

On June 9, 2021, QAD entered into a confidentiality agreement with Party G. Such confidentiality agreement did not include any standstill provisions.

On June 14, 2021, Morgan Stanley relayed that Thoma Bravo had communicated that, as a result of its further diligence, Thoma Bravo’s final proposal that it would submit the next day on June 15, 2021 would likely be at a lower price per share than the initial price of $90 per share set forth in its preliminary indication of interest submitted on May 11, 2021.

The Special Committee and its advisors also discussed an approach regarding the Special Committee’s review of any proposals submitted on June 15, 2021, and determined that no terms should be shared with Ms. Lopker until the Special Committee has reviewed such proposals with its advisors and has formed an independent view on the proposals. The Special Committee also confirmed that it had made clear to Ms. Lopker and the potential counterparties that the Special Committee must first agree to a price per share and any other terms that are fair to all stockholders with a potential counterparty before any negotiations may take place between such counterparty and Ms. Lopker and that, if Ms. Lopker sought a rollover of any shares, then a vote of the majority of the minority of QAD stockholders would be required.

On June 15, 2021, Thoma Bravo’s proposal lowered its offer price as compared to its earlier preliminary indication of interest — from $90 per share to $85 per share, due to its view of findings in its recent diligence. Thoma Bravo’s offer proposed that Ms. Lopker may roll $150 million of her shares (valued at $85 per share) and explicitly stated that its proposal, including the price per share in connection with the merger, was not premised or conditioned on any rollover or the terms of such rollover. Thoma Bravo indicated that it was ready to execute a definitive agreement in as soon as 72 hours and only had confirmatory due diligence left to complete. On June 15, 2021 QAD’s closing share price of Class A Common Stock was $77.00.

On June 16, 2021, Morgan Stanley received a proposal and representatives of Paul, Weiss received a revised draft merger agreement, each from Party B, which were promptly shared with the Special Committee and its advisors. Party B’s proposal included an offer price of approximately $86 per share, just as it had in its preliminary indication of interest. Party B’s offer invited Ms. Lopker to roll a portion of her shares, stating that Party B proposed a minimum rollover of 30% and a maximum of 50% of Ms. Lopker’s shares, and included a term sheet that described certain stockholder rights in connection with the securities Ms. Lopker would receive in a rollover. Party B’s proposal indicated that it had due diligence left to complete and would likely require about three more weeks before it would be in a position to execute a definitive agreement, and that the terms of its offer remain subject to ongoing diligence. On June 16, 2021, QAD’s closing share price of Class A Common Stock was $78.03.

Also on June 16, 2021, After discussion and deliberation, the Special Committee directed representatives of Morgan Stanley to communicate to Thoma Bravo and Party B that they would need to increase their respective offer prices, and also that Party B should proceed more quickly than communicated in its proposal and that, subject to any future discussions with Ms. Lopker, Thoma Bravo may need to consider altering the terms of their rollover proposal, and to reiterate to both that a rollover of any of Ms. Lopker’s shares would require a “majority of the minority” stockholder vote, and such vote would be a non-waivable condition for the merger. The members of the Special Committee and representatives of Paul, Weiss had further discussion during an executive session of the meeting.

Over the course of the period from June 16, 2021 to June 21, 2021, and at the direction of the Special Committee, representatives of Morgan Stanley had a number of discussions with each of Thoma Bravo and Party B, communicating that such parties should increase their respective offer prices and that Party B should expedite timing to get to a definitive agreement.

On June 18, 2021, at the direction of the Special Committee, representatives of Morgan Stanley communicated to Thoma Bravo that the Special Committee requested that it increase its offer price to $92 per share, which Thoma Bravo stated it was not willing to do. On June 18, 2021, QAD’s closing share price of Class A Common Stock was $72.93.

On June 19, 2021, after further discussion with representatives of Morgan Stanley, Thoma Bravo informed representatives of Morgan Stanley that it was willing to increase its offer price to $87.50 per share, and indicated that this represented Thoma Bravo’s best and final offer. Such revised offer was promptly shared with the Special Committee and its advisors. On June 18, 2021, the last full trading day prior to June 19, 2021, QAD’s closing share price of Class A Common Stock was $72.93.

On June 19, 2021, Ms. Lopker informed the Special Committee that she had retained Moelis & Company as her financial advisor.

On June 21, 2021, as disclosed in a Form 8-K filed by the Company with the SEC on April 29, 2021, Mr. Roberts’s term on the QAD Board (and therefore Special Committee) ended pursuant to the term set forth in the bylaws of the Company, and he did not stand for reelection.

On June 21, 2021, Party B communicated to representatives of Morgan Stanley that it was withdrawing its offer as it would not increase its price, which was still at approximately $86 per share, and nor would it expedite the timeline for diligence. Such communication was promptly provided to the Special Committee and its advisors.

Later on June 21, 2021, The Special Committee discussed potential steps it might take to persuade Party B to change its decision and re-engage in the process. Representatives of Morgan Stanley provided an update regarding Party G, the one additional potential counterparty still engaged in the process, noting that such party had not submitted an offer and had not indicated that it was interested in moving forward. Later that day, representatives of Morgan Stanley, at the direction of the Special Committee, again contacted Party G to encourage it to submit a bid.

In that same meeting, the Special Committee and its advisors discussed Thoma Bravo’s revised offer at $87.50 per share, including whether there was an opportunity to further increase the price given the negotiations over the prior week and Thoma Bravo’s statement that this was its “best and final” offer. The Special Committee and its advisors also discussed the fairness of the Thoma Bravo proposal’s price and terms to stockholders not affiliated with the Lopker Entities, and that it was an attractive offer. After further discussion and deliberation with its advisors, the Special Committee directed representatives of Morgan Stanley to communicate to Thoma Bravo, that subject to other terms and conditions, the Special Committee would be willing to recommend a transaction at $87.50 per share if such transaction included Thoma Bravo providing a full equity commitment in connection with the financing of the transaction, and no financing contingency.

On June 23, 2021, representatives of Morgan Stanley, at the direction of the Special Committee, contacted Party G again to encourage it to submit a bid.

On June 24, 2021, Party G indicated to representatives of Morgan Stanley that it would no longer be participating in the process.

On June 24, 2021, the Special Committee met, along with representatives of Paul, Weiss and Morgan Stanley, to discuss the status of the process. The Special Committee also discussed Ms. Lopker’s role at QAD following the closing of the potential transaction with Thoma Bravo, and terms being negotiated between her and Thoma Bravo, including Ms. Lopker seeking that a certain amount of her shares participate in a rollover. The Special Committee and its advisors discussed such topics as well as status of the draft merger agreement, key terms and other open issues.

On June 25, 2021, Representatives of Morgan Stanley stated that, after extensive negotiations, Thoma Bravo indicated that it would agree to provide a full equity commitment in connection with the financing of the transaction which would eliminate the need for Thoma Bravo to secure debt financing and enhance the certainty of closing the proposed transaction. The Special Committee and its advisors discussed the same, and the Special Committee directed Paul, Weiss to revise the documents to reflect, among other terms, such full equity commitment and a supporting guarantee from TB Fund XIV L.P., an affiliate of Thoma Bravo, L.P.

At that same meeting, the Special Committee and its advisors discussed other developments in the market, including the recently announced proposed acquisition of Plex Systems by Rockwell Automation, including the revenue multiple and other terms obtained in the Plex Systems transaction and discussed factors that differentiated Plex Systems from QAD, including, among other factors, Plex System’s business in Industrial IOT, growth and margin profile, the fact that Plex Systems has 500 employees and its operations are U.S.-based, and the synergies created through acquisition by a strategic counterparty. The members of the Special Committee and representatives of Paul, Weiss had further discussion during an executive session of the meeting.

Also during the course of the day on June 27, 2021, the Special Committee, the Company, Thoma Bravo and Ms. Lopker and their respective representatives exchanged multiple drafts of the support agreement and engaged in related negotiations.

Separately, during the day on June 27, 2021, Ms. Lopker and Thoma Bravo and their respective representatives exchanged multiple drafts of the contribution and exchange agreement and related documents, which were also shared with the Special Committee and its advisors.

Later in the day on June 27, 2021, Representatives of Morgan Stanley reviewed Morgan Stanley’s financial analysis of the transactions and rendered its oral opinion, subsequently confirmed in writing, that, as of June 27, 2021, and based upon and subject to the assumptions made, procedures followed, matters considered and qualifications and limitations on the scope of review undertaken by Morgan Stanley as set forth in its written opinion, the Merger Consideration to be received by the Company’s stockholders (other than the holders of the Excluded Shares) pursuant to the Merger Agreement was fair from a financial point of view to such stockholders in the aggregate. Following discussion, the Special Committee unanimously (i) determined that the Merger Agreement and the transactions contemplated thereby, including the Merger, are advisable, fair to, and in the best interests of, the Company and the Company’s stockholders; (ii) recommended that the QAD Board approve the Merger Agreement and the transactions contemplated thereby, including the Merger, and declare the Merger Agreement and the transactions contemplated thereby, including the Merger, advisable, fair to and in the best interests of the Company and the Company’s stockholders; and (iii) recommended that, subject to approval by the QAD Board, the QAD Board resolve to recommend that the holders of shares vote to adopt the Merger Agreement and approve the transactions contemplated thereby, including the Merger.

Immediately following the meeting of the Special Committee on June 27, 2021, the QAD Board (other than Ms. Lopker, who recused herself) met, along with representatives of Paul, Weiss and Morgan Stanley. The Special Committee delivered its recommendation to the QAD Board. Following discussion, based on the unanimous recommendation of the Special Committee, the QAD Board (other than Ms. Lopker, who recused herself), among other things (i) determined that the Merger Agreement and the transactions contemplated thereby, including the Merger, are advisable, fair to, and in the best interests of, the Company and the Company’s stockholders; (ii) adopted and approved the Merger Agreement and the transactions contemplated thereby, including the Merger; (iii) directed that the Merger Agreement be submitted to the holders of shares for their adoption and approval; and (iv) resolved to recommend that the holders of shares vote to adopt the Merger Agreement and approve the transactions contemplated thereby, including the Merger.

Later in the evening on June 27, 2021, the Special Committee, the Company and Thoma Bravo and their respective representatives put into execution form the Merger Agreement and related transaction documents, and, such parties along with Ms. Lopker and representatives of Paul Hastings, put into execution form the Support Agreement. Also during this time, Ms. Lopker and Thoma Bravo and their respective representatives, put into execution form the Contribution and Exchange Agreement and related documents. Thereafter, the Support Agreement, Merger Agreement and related transaction documents and Contribution and Exchange Agreement and related documents were executed and delivered by the relevant parties. For additional information regarding the final terms of the Merger Agreement, see the section entitled “The Merger Agreement” and the copy of the Merger Agreement attached as Annex A to this proxy statement. For additional information regarding the final terms of the Support Agreement, see the section entitled “Support Agreement” and the copy of the Support Agreement attached as Annex B to this proxy statement. For additional information regarding the final terms of the Contribution and Exchange Agreement, see the section entitled “Contribution and Exchange Agreement” and the copy of the Contribution and Exchange Agreement attached as Annex C to this proxy statement.

Prior to the opening of equity trading markets in the United States on June 28, 2021, QAD issued a press release announcing the signing of the Merger Agreement with an affiliate of Thoma Bravo.